When it comes to acquiring a vehicle, one of the most common questions drivers face is whether they should lease or buy. Each option offers its own set of advantages and drawbacks, and the right choice depends on a variety of factors, including your financial situation, driving habits, and long-term goals. In this article, we’ll compare the pros and cons of leasing and buying a car to help you make an informed decision that best suits your needs.

Understanding the Basics of Leasing and Buying

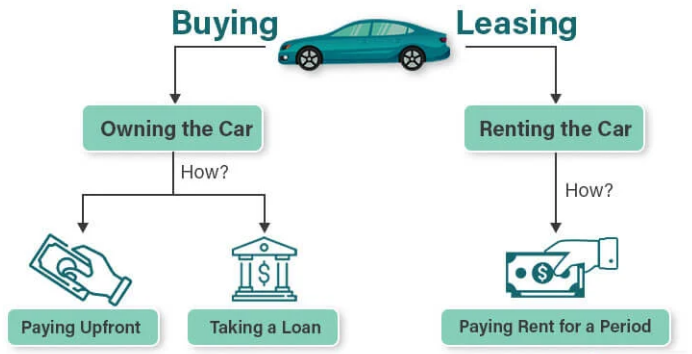

Before diving into the details, it’s important to understand the key differences between leasing and buying a car:

- Leasing is essentially renting a car for a set period (usually 2-4 years) with the option to purchase it at the end of the lease term. You make monthly payments for the vehicle, but you don’t own it during the lease. At the end of the lease, you return the car or buy it for a predetermined residual value.

- Buying means you own the car outright after financing it (either through a loan or paying the full price upfront). Monthly payments are typically higher compared to leasing, but at the end of the loan term, you own the vehicle.

Now, let’s break down the pros and cons of each option in more detail.

Pros and Cons of Leasing a Car

Pros of Leasing

- Lower Monthly Payments: One of the biggest draws of leasing is the lower monthly payments. When you lease a car, you are essentially paying for the car’s depreciation during the lease period, rather than its entire value. This often results in monthly payments that are lower than if you were to buy the car with a loan.

- Newer Car Every Few Years: Leasing allows you to drive a new car every few years. Lease terms typically last between 2-4 years, and once the lease expires, you can upgrade to a new model with the latest technology, features, and design.

- Lower Repair Costs: Since most leased cars are under warranty for the duration of the lease, you’ll likely be covered for most major repairs. While you’ll still need to handle routine maintenance like oil changes and tire rotations, significant repair costs are generally not your responsibility.

- Less Upfront Cost: Leasing a car typically requires less upfront cash than buying. You may be required to make a down payment, but it’s usually smaller than the down payment required for purchasing a car.

Cons of Leasing

- No Ownership: One of the biggest drawbacks of leasing is that you don’t own the car. At the end of the lease, you have no equity in the vehicle, meaning all the money you spent on the lease is essentially gone.

- Mileage Limits: Lease agreements often come with mileage limits, typically ranging from 10,000 to 15,000 miles per year. If you exceed the mileage limit, you may face expensive penalties. If you drive long distances regularly, leasing may not be the best option.

- Customization Restrictions: Leased cars are not yours to modify. You can’t add custom features, paint jobs, or aftermarket accessories without violating the terms of the lease. This can be a limitation for drivers who like to personalize their vehicles.

- Wear and Tear Charges: Leases require you to maintain the vehicle in good condition. If the car shows signs of excessive wear and tear, you may be charged additional fees at the end of the lease term. This includes things like dents, scratches, or interior damage.

Pros and Cons of Buying a Car

Pros of Buying

- Ownership and Equity: When you buy a car, you own it outright once the loan is paid off. This means you have equity in the vehicle, and once the loan term is over, your monthly payments stop. Afterward, the car becomes an asset that you can sell or trade in for another vehicle.

- Unlimited Mileage: Unlike leasing, when you buy a car, there are no mileage restrictions. This makes buying a great option for those who drive long distances regularly or plan to keep the vehicle for many years.

- Flexibility and Customization: As the owner of the vehicle, you have the freedom to modify it as you wish. Whether you want to add new features, paint the car a different color, or install aftermarket accessories, you are free to do so without worrying about violating any terms.

- Long-Term Cost Savings: While monthly payments for buying are higher than leasing, over the long term, buying can be more economical. Once the loan is paid off, you no longer have any car payments, which can save you money in the future. Additionally, if you keep the car for a long time, the overall cost of ownership can be lower than leasing multiple vehicles over the years.

Cons of Buying

- Higher Monthly Payments: Buying a car typically results in higher monthly payments compared to leasing because you’re paying for the entire vehicle, not just its depreciation. This may make buying less appealing for those on a tight budget.

- Larger Down Payment: When buying a car, you may be required to make a larger down payment than you would for a lease. While some financing options offer low or no down payment, putting down a significant amount upfront may strain your finances.

- Depreciation: As soon as you drive a new car off the lot, its value begins to depreciate. After a few years, the car may lose a significant portion of its value, and if you choose to sell or trade it in, you may not recoup as much as you paid.

- Maintenance Costs: While you own the car, you are responsible for all maintenance and repair costs, which can become more expensive as the car ages. After the manufacturer’s warranty expires, you may need to pay out of pocket for repairs and upkeep.

Financial Comparison: Leasing vs. Buying

To better understand the financial implications of leasing versus buying, it’s helpful to break down the costs:

- Leasing: Leasing typically results in lower monthly payments. However, over the long term, leasing may cost more because you are constantly paying for new cars without building any equity. Lease payments may also come with additional charges like down payments, taxes, and fees for excess wear and tear or mileage overages.

- Buying: While monthly payments for buying a car are generally higher, once the loan is paid off, you own the car and can continue driving it without making payments. Additionally, if you keep the car for several years, you can minimize the cost of ownership by avoiding the need to buy a new car every few years.

Which Option is Right for You?

The decision to lease or buy ultimately depends on your individual needs, preferences, and financial situation. Here are some key factors to consider when deciding:

Leasing Might Be Right for You If:

- You prefer driving a new car every few years.

- You want lower monthly payments and don’t mind not owning the vehicle.

- You don’t drive excessively (i.e., fewer than 12,000-15,000 miles per year).

- You want a vehicle under warranty for most of the time.

- You like the idea of a predictable payment structure with fewer long-term responsibilities.

Buying Might Be Right for You If:

- You plan to keep the car for many years and want to build equity.

- You drive long distances or frequently go over mileage limits.

- You want the freedom to customize your vehicle.

- You prefer to avoid the hassle of mileage restrictions, wear and tear charges, and vehicle return processes.

- You are comfortable with higher monthly payments but want a more cost-effective option in the long term.

Conclusion

Leasing and buying both offer unique advantages depending on your priorities and lifestyle. Leasing is great for those who want to drive a new car every few years and enjoy lower monthly payments, while buying is ideal for those who want to own a car and keep it for an extended period. Carefully evaluate your financial situation, driving habits, and long-term goals before making a decision. Whichever option you choose, it’s important to consider the overall costs, potential benefits, and long-term implications on your financial health.